Tron Industry Weekly Report: Federal Reserve Policy Expectations Fluctuate, BTC Continues the "60,000 Defense Battle," Detailed Analysis of Institutional-Level Quantitative Trading and On-Chain Derivatives Market Variation

This week, the macro core will focus on the re-pricing of U.S. economic data and global monetary policy expectations. RWA and stablecoins continue to be the core theme, especially with the institutional adoption of government bonds, money market funds, and gold-backed tokenized assets, which strengthens the narrative of "on-chain real yield assets."

This week, the macro core will focus on the re-pricing of U.S. economic data and global monetary policy expectations. RWA and stablecoins continue to be the core theme, especially with the institutional adoption of government bonds, money market funds, and gold-backed tokenized assets, which strengthens the narrative of "on-chain real yield assets."I. Outlook

1. Macroeconomic Summary and Future Predictions

Last week, the global macro environment continued the "weak growth + resilient inflation" combination typical of a high interest rate cycle. In the United States, economic data remained resilient; although the job market showed signs of marginal cooling, it did not significantly deteriorate. The pace of inflation decline has slowed, leading the Federal Reserve to maintain a "wait-and-see" policy stance, with market expectations for interest rate cuts further delayed. The dollar index remained high and volatile, while the U.S. Treasury yield curve showed a phased recovery from inversion but has not fully normalized, indicating that market expectations for long-term growth remain cautious. In Europe, economic growth momentum continued to weaken, with manufacturing and external demand being the main drag, but inflation has entered a relatively controllable range, shifting the policy focus from anti-inflation to stabilizing growth. In emerging markets, overall differentiation has intensified, with capital flows favoring economies with stronger fundamentals and robust foreign exchange reserves. The global macro landscape remains in a "rebalancing phase after a high interest rate maintenance period."

This week, the macro focus will center on U.S. economic data and the repricing of global monetary policy expectations. In the U.S., the market will closely watch for further signs of cooling in employment, inflation, and consumption-related data, which will directly affect the Fed's judgment on the "duration of high interest rates." If data continues to show resilience, global liquidity expectations will likely remain tight; if clear signs of weakness emerge, the market may preemptively trade on easing expectations. In Europe, economic data will continue to verify whether growth weakness has bottomed out, but short-term policies will still focus on stability, making a radical shift unlikely. Overall, the global macro environment remains in a "window of uncertainty at the tail end of high interest rates," with market volatility primarily driven by expectation differences rather than directional trend changes.

2. Market Movements and Warnings in the Crypto Industry

This week, the crypto market continued its weak fluctuations and structural differentiation. Bitcoin hovered around $60,000; although long-term holders continued to accumulate, ETF capital flows remained unstable, reflecting that institutional funds are still in a wait-and-see phase. On a macro level, risk assets faced overall pressure, with geopolitical uncertainties and fluctuating Fed policy expectations causing crypto assets to exhibit increased volatility alongside the U.S. tech sector, with market risk appetite not showing significant recovery. Meanwhile, funds continued to migrate from the crypto market to AI and tech assets, further suppressing short-term upward momentum.

Next week, the core variables in the market will focus on U.S. macro data and global liquidity expectations, which will directly influence the Fed's future interest rate path judgment, thereby determining the overall direction of risk assets. If the data is strong, it may reinforce expectations for "higher rates for longer," putting pressure on the crypto market; if the data weakens, it could open a window for a short-term rebound in risk assets. In terms of the crypto market itself, it is expected to maintain a range-bound fluctuation + structural market, with BTC likely continuing to fluctuate around key support levels. The market's main focus remains on ETF capital flows, long-term holder behavior, and changes in macro interest rate expectations. In the absence of incremental liquidity and strong narrative drivers, the overall trend is more defensive.

3. Industry and Sector Hotspots

RWA and stablecoins continue to be the core themes, especially with institutional adoption of tokenized assets like government bonds, money market funds, and gold-related assets, strengthening the narrative of "on-chain real yield assets." In DeFi, the focus is on yield optimization and risk restructuring (such as structured yields, cross-chain liquidity, and institutional-level lending), while cross-chain infrastructure and intent-based protocols continue to optimize execution efficiency. At the same time, AI × Crypto (Agent, payments, automated trading) continues to heat up, but remains more focused on infrastructure and standard protocol exploration. Overall, the market is evolving from a "high Beta speculative cycle" to a mid-cycle structure of RWA + stable yields + infrastructure reconstruction.

II. Market Hotspot Sectors and Potential Projects of the Week

1. Overview of Potential Projects

1.1. Detailed Explanation of Total Financing of $61.8 Million, Led by Dragonfly and Bain Capital, with Participation from HackVC, Mirana, and North Island — High-Performance Financial Infrastructure Variational for Institutional-Level Quantitative Trading and On-Chain Derivatives Market

Introduction

Variational is a protocol for on-chain derivatives trading, covering multiple markets including cryptocurrencies, stocks, commodities, and foreign exchange.

Its core goal is to aggregate the deepest possible liquidity sources from each market, including:

Centralized Exchanges (CEX)

Decentralized Exchanges (DEX)

Traditional financial market makers and liquidity providers (TradFi Dealers)

Thus, connecting DeFi directly with the global financial market.

Currently, the Variational Protocol mainly supports two core products:

Omni

A zero-fee perpetual contract trading platform that provides users with an efficient on-chain derivatives trading experience.

Pro

A settlement layer for institutional users that supports the creation, trading, and settlement of customized derivatives products.

Overall, Variational aims to expand the on-chain derivatives market beyond crypto assets by unifying liquidity and settlement infrastructure, covering traditional financial markets such as stocks, commodities, and foreign exchange, achieving deep integration of DeFi and global capital markets.

Protocol Framework Overview

- Variational Protocol

The Variational Protocol is a derivatives trading protocol composed of both on-chain and off-chain infrastructure, designed to automate the quoting, clearing, and settlement processes of derivatives trading.

Users typically do not interact directly with the underlying protocol but trade through applications built on Variational, such as:

Omni (zero-fee perpetual contract platform)

Pro (institutional-level customized derivatives settlement platform)

All applications built on Variational share the following core infrastructure.

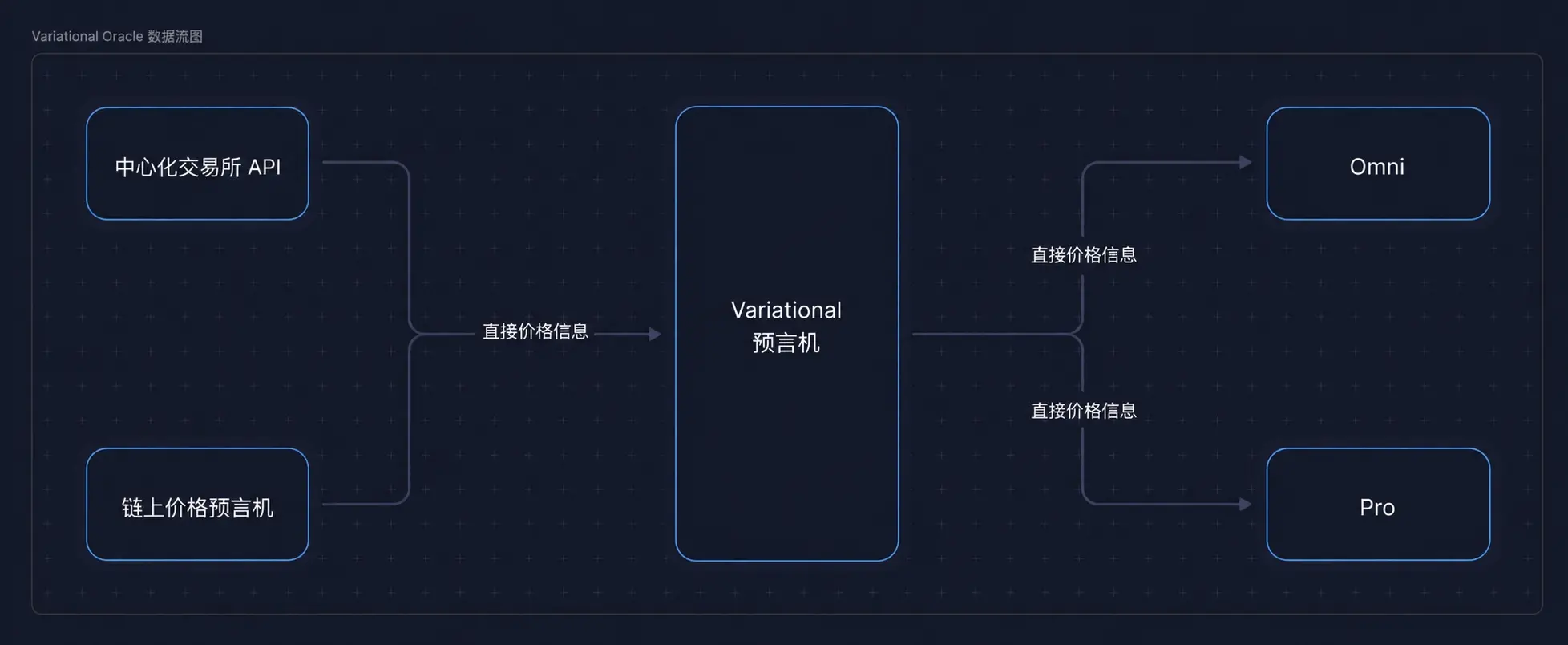

Pricing Oracle

Variational uses a self-developed pricing oracle to provide reliable market price data for various assets.

Its price sources include multiple partner data providers and aggregate:

Centralized Exchange (CEX) data

Decentralized Exchange (DEX) data

The system calculates the "fair price" of assets based on this market data.

Therefore, the core premise for trading a certain asset on Variational is:

There is a reliable price data source

A reasonable price calculation model can be established

Core Margin & Liquidation Engine

This module is responsible for managing trading margins and position liquidations.

Main functions include:

Real-time calculation of maintenance margin requirements

Monitoring position risk levels

Automatically liquidating positions with insufficient margins

Its liquidation mechanism operates in a Settlement Pool mode.

In other words:

👉 When a user's position is liquidated, it does not affect other traders in the settlement pool.

Thus, reducing systemic risk.

Settlement & Funding Rate Engine

This module is mainly responsible for:

Calculating the settlement price at contract expiration

Calculating the funding rate

Tracking the funding fee payment situation between both parties in the trade

For products like Pro that support customized derivatives, this module undertakes complete settlement functions.

Since Omni focuses on perpetual contract trading, it only uses the funding rate part and does not involve expiration settlement.

On-Chain Transaction Handler

Transactor

Responsible for submitting all necessary on-chain transactions.

In Omni, it mainly undertakes:

User deposit and withdrawal transaction submissions

OLP fund pool asset transfers

New settlement pool fund allocations

It can also pay part of the on-chain gas costs on behalf of users to optimize the trading experience.

Watcher

The Watcher is used to monitor the status of all on-chain transactions.

Its main functions include:

Confirming whether transactions are ultimately completed

Preventing fake deposits

Preventing vampire deposits

Ensuring platform balances are consistent with on-chain assets

Thus ensuring the security and accuracy of the entire trading system.

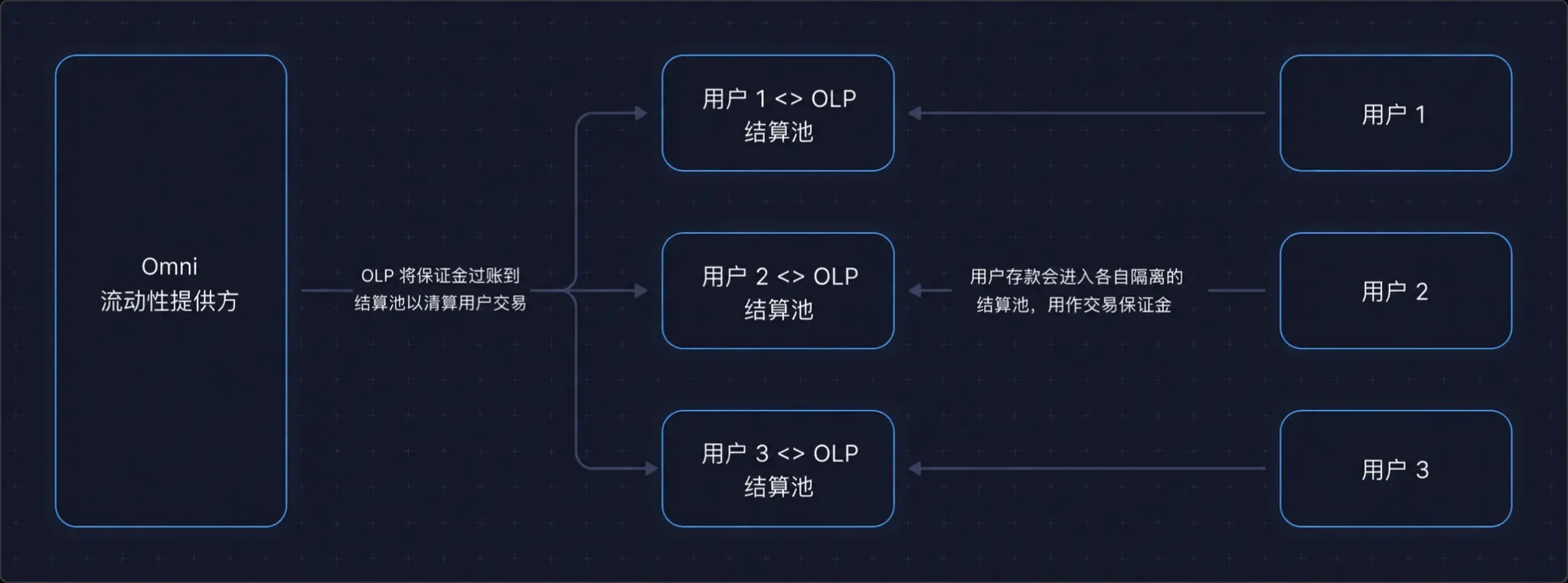

- Omni Liquidity Provider (OLP)

The Omni Liquidity Provider (OLP) is the core liquidity provision system of the Omni platform and is also the unified counterparty for all trades on Omni.

Unlike traditional derivatives trading platforms that rely on external market makers, Omni independently assumes all market-making responsibilities through OLP.

OLP consists of three main parts:

Vault

Market Making Engine

Risk Management System

The Vault

The Vault is a smart contract that holds OLP funds, primarily storing USDC.

Its functions include:

Providing margin support for OLP

Serving as the counterparty fund pool

Accumulating market-making profits

Essentially, it is the funding infrastructure for the entire OLP.

The Market Making Engine

OLP operates a self-developed high-frequency market-making system.

This system analyzes market data in real-time from:

CEX (Centralized Exchanges)

DEX (Decentralized Exchanges)

TradFi (Traditional Financial Markets)

Including:

Order flow

Volatility

Market depth

To calculate fair asset prices and continuously provide quotes.

Its core goal is to achieve continuous profitability while maintaining the smallest possible bid-ask spread.

This market-making system has been iteratively developed based on the Variational team's over 7 years of market-making experience.

The Risk Management System

To avoid taking on excessive directional risk, OLP utilizes self-developed algorithmic strategies for dynamic risk management.

Mainly includes:

Position risk monitoring

Hedging

Yield optimization

By hedging some risk exposure through external markets, it improves long-term capital efficiency and stability.

OLP as the Sole Counterparty

In every trade on Omni:

The user is one party in the trade

OLP is the other party

Both parties need to maintain margins and are subject to unified margin rules.

If margins are insufficient:

The user may be liquidated

OLP may also trigger a risk management mechanism

This design is significantly different from traditional derivatives platforms.

Core Advantages Brought by OLP

Zero Fees

Since the platform does not rely on external market makers for liquidity, Omni does not need to pay incentives to market makers through trading fees.

This is also a key reason why Omni can achieve zero trading fees.

Listing Variety

The conditions required for OLP to launch new markets are relatively simple:

Reliable price sources

Quoting models

Risk hedging mechanisms

Thus enabling rapid support for trading.

As a result, Omni currently supports around 500 trading markets and has the capacity to further expand to:

RWA (Real World Assets)

Exotic Markets

More traditional financial products

How Does OLP Make Profit?

The profit process for OLP is as follows:

Continuously calculate reasonable spreads for each asset

Users trade at OLP's quoted prices

OLP assumes the role of counterparty

If necessary, hedge risks through external markets

Earn profits from the bid-ask spread

Thus, OLP's core revenue source is not transaction fees, but:

Market Making Spread.

How Does the Variational Protocol Make Profit?

The Variational protocol itself does not charge users transaction fees directly.

Its revenue comes from the spread profits earned by OLP.

Currently, the mechanism is:

OLP receives all spread income

20% of this is automatically allocated to the Variational Protocol Treasury

The remaining portion stays within the OLP system for liquidity and profit accumulation

- Variational Pro (Institutional-Level OTC Derivatives Platform)

Variational Pro is an OTC derivatives trading and settlement platform designed for institutional investors, supporting the quoting, trading, clearing, and settlement of various customized derivatives products. Its core goal is to fully chain and automate the OTC trading process, which traditionally relies on Telegram, email, manual reconciliation, and offline agreements.

Currently, a large amount of institutional-level crypto derivatives trading still relies on manual processes, including KYC, ISDA agreement signing, off-exchange inquiries, manual margin management, and post-trade settlement, which not only lacks efficiency but also carries a high risk of human error and counterparty risk. Variational Pro allows institutions to directly publish trading needs through a unified RFQ (Request For Quote) mechanism, simultaneously obtaining competitive quotes from multiple market makers, thereby improving price transparency and liquidity.

Once a trade is agreed upon, both parties' funds are directly deposited into an on-chain smart contract escrow account (Settlement Pool), and the system automatically completes margin management, funding rate calculation, settlement, and clearing without manual intervention. The entire trading lifecycle from inquiry, execution to settlement is automatically executed by the protocol, significantly reducing operational costs and counterparty risks.

Its core features include:

RFQ inquiry mode: Multiple market makers compete for quotes, enhancing price transparency.

Bilateral OTC trading structure: Both parties trade directly, with risks isolated in an independent Settlement Pool.

High customization: Supports custom margin rules, clearing mechanisms, trading structures, and designated counterparties.

On-chain automatic settlement: Automatically handles margin monitoring, fund transfers, and clearing processes.

Supports any asset derivatives: Not limited to mainstream crypto assets, but can also extend to altcoins and other complex structured products.

Core Positioning

Variational Pro is essentially an on-chain OTC derivatives trading and settlement infrastructure aimed at upgrading the traditional OTC derivatives market, which heavily relies on manual operations, to a transparent, automated, and programmable on-chain financial system.

Tron Commentary

Variational's advantage lies in its attempt to build a unified on-chain derivatives infrastructure covering cryptocurrencies, stocks, foreign exchange, and commodities, connecting DeFi with global capital markets by aggregating liquidity from CEX, DEX, and traditional financial institutions. Its Omni platform adopts the OLP unified market-making model to achieve zero-fee perpetual contract trading and coverage of approximately 500 trading markets, while Pro automates the processes in traditional institutional OTC derivatives trading that rely on Telegram, email, and manual settlement, significantly reducing counterparty risk and operational costs, possessing strong institutional-level financial infrastructure attributes.

However, its disadvantage lies in the overall architecture being highly complex, with strong reliance on market-making capabilities, risk hedging models, oracle pricing, and external liquidity. Especially, while OLP as a unified counterparty improves liquidity efficiency, it may also concentrate some systemic risks within a single market-making system. Additionally, the institutional OTC market itself heavily relies on real institutional adoption, and whether it can continue to attract large market makers, funds, and TradFi liquidity access remains a key challenge for its long-term development.

2. Detailed Explanation of Key Projects of the Week

2.1. Detailed Explanation of Total Financing of $13.5 Million, Led by Polychain & North Island, with Participation from Ripple, Borderless, and Fabric — Building Cross-Chain Liquidity and Execution Infrastructure with Full Chain Interoperability Squid

Introduction

Squid is a unified cross-chain infrastructure integration layer that enables seamless cross-chain swaps, bridging, and contract calls, currently covering over 100 blockchains.

Execution speed of under 5 seconds

Based on the Squid Intents architecture, it achieves rapid confirmation of cross-chain transactions and executions, with an average execution time of less than 5 seconds.

Over $6 billion in cross-chain transaction volume

As of now, Squid has safely processed:

Over $6 billion in transaction volume

Over 4 million cross-chain transactions

Validating the stability and security of its infrastructure.

Multiple integration methods

Developers can choose from:

Widget

API

SDK

To quickly access cross-chain capabilities.

Customizable cross-chain contract calls

Through the Hooks mechanism, developers can not only complete cross-chain transfers but also automatically execute any on-chain operations on the target chain.

For example:

Automatically staking after a swap

Automatically depositing into a DeFi protocol after a swap

Automatically purchasing NFTs after a swap

Achieving true cross-chain business combinations.

Core System Architecture Analysis

Liquidity Model

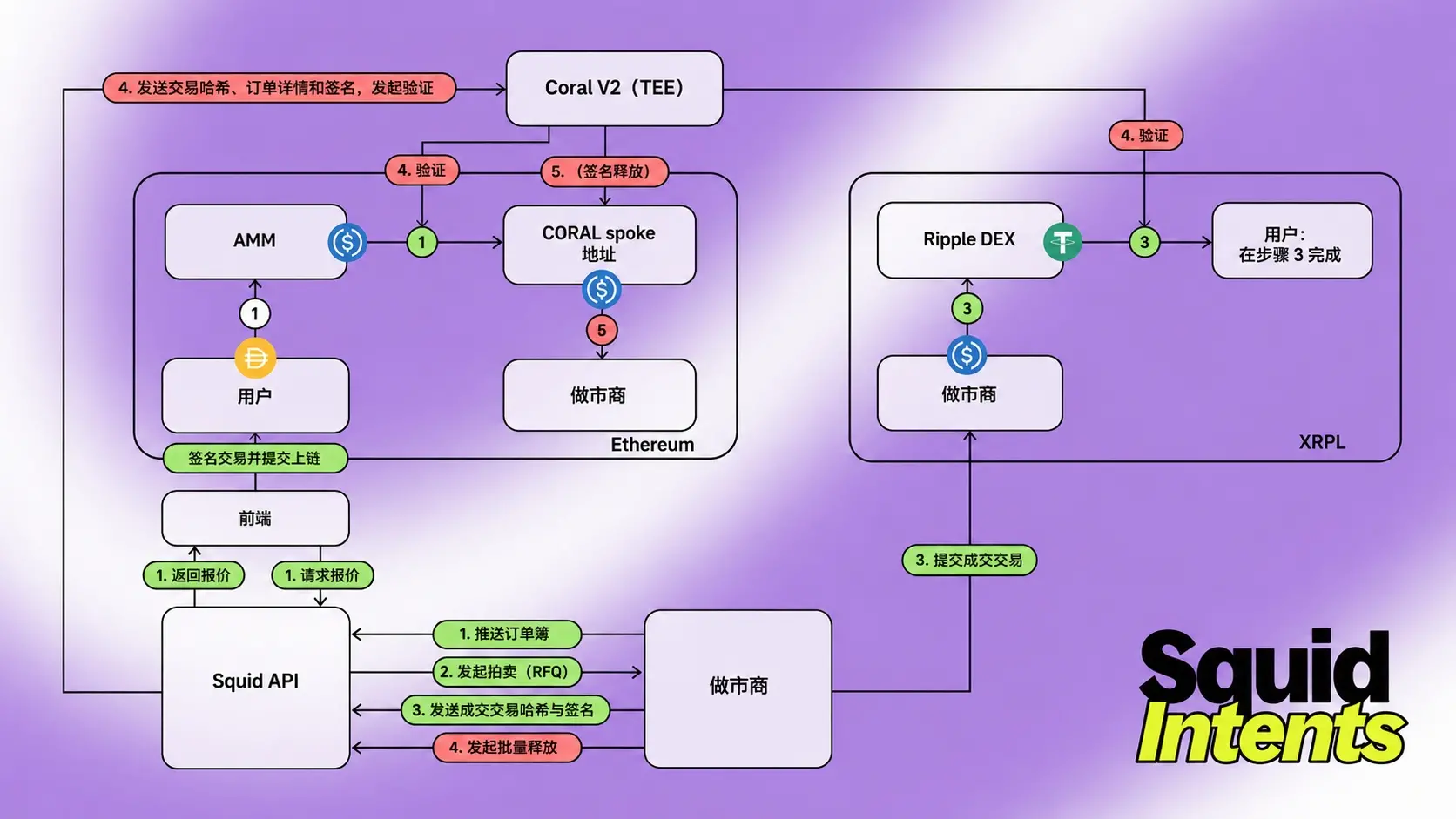

With the launch of Squid Intents, Squid's liquidity model has been upgraded, utilizing a post-deposit RFQ (Request For Quote) bidding mechanism and a TEE (Trusted Execution Environment) validated batch settlement system, enhancing transaction execution quality while reducing on-chain complexity.

Unlike traditional cross-chain bridges that rely on AMM liquidity pools, Squid Intents no longer completes transactions through fixed liquidity pools but instead uses a market-based bidding mechanism to obtain optimal liquidity.

Its goals are to achieve:

Better prices

Lower slippage

Higher liquidity efficiency

Broader cross-chain asset support

RFQ Auctions

When a user initiates a cross-chain swap:

User funds are first deposited into the source chain

Squid Intents initiates RFQ bidding on the source chain

Multiple market makers participate in competitive quoting

The system selects the optimal quote's Solver (executor)

The Solver directly completes asset delivery on the target chain

The Solver then conducts risk hedging independently

Thus, the user receives the real optimal market price at the time of execution rather than a pre-estimated quote that includes volatility buffers.

Offchain Coordination, Onchain Settlement

Squid Intents performs the majority of execution logic off-chain.

All matching, bidding, and execution coordination operate within Squid's TEE verification infrastructure.

Only the most necessary parts are retained on-chain:

Asset transfers

Final settlements

The advantages of this approach include:

Significantly reduced gas costs

Decreased on-chain computational burden

Avoiding slippage risks caused by AMM routing

Essentially, transaction coordination is completed off-chain, while the on-chain system is responsible for the final asset delivery.

Any Token, Any Chain

The liquidity of Squid Intents comes from cross-chain liquidity provided natively by market makers, rather than relying on:

Wrapped Assets

Synthetic Assets

Therefore, Squid can support:

Any token

Any supported chain

Including networks that some traditional cross-chain protocols find difficult to cover, such as:

Bitcoin

Solana

XRPL (Ripple)

And other non-EVM ecosystems.

Transaction Times & Fees

Fees

Currently, Squid does not charge protocol fees; users only need to pay the actual gas fees for the source and target chains.

Partners integrating via the Squid API or SDK can set their own service fees, from which Squid receives a share.

Source Chain Transactions

EVM Chains:

Fees mainly include:

Gas required for Swap, Transfer, Approve

Target chain execution fees

All paid in the source chain's native gas token.

Cosmos Chains:

Target chain execution fees will be directly deducted from the bridged assets, and the IBC relay process is free, so overall costs are usually lower.

Cross-chain Message Fees

If the transaction involves a target chain swap, cross-chain message transmission fees will also be incurred.

This fee is charged by the Axelar Relayer network for completing cross-chain message verification and execution.

Squid will automatically calculate the fees users need to pay on the source chain based on real-time gas pricing provided by Axelar, eliminating the need to prepare target chain gas in advance.

Tron Commentary

Squid's advantage lies in its positioning as a unified cross-chain infrastructure layer, integrating cross-chain swaps, bridges, and contract calls into a single interface through Squid Intents, RFQ bidding mechanisms, and TEE verified execution environments, supporting over 100 chains (including Bitcoin, Solana, XRPL, and other non-EVM ecosystems), and replacing traditional liquidity pool models with competitive quotes from market makers to achieve better prices, lower slippage, and faster cross-chain execution, while supporting any token across any chain, providing strong cross-chain expansion capabilities for wallets, DEXs, and DeFi protocols.

However, its disadvantage lies in the system's heavy reliance on external market maker liquidity, TEE infrastructure, and the stable operation of cross-chain messaging networks (such as Axelar). Some core execution logic also occurs off-chain, which, while improving efficiency, introduces certain trust assumptions compared to fully on-chain solutions. Additionally, competition in the cross-chain infrastructure sector is fierce, and it will need to continuously expand its liquidity network and ecosystem integration scale to maintain its advantages.

III. Industry Data Analysis

1. Overall Market Performance

1.1. Spot BTC vs ETH Price Trends

BTC

ETH

IV. Macroeconomic Data Review and Key Data Release Points for Next Week

1. Review of Macroeconomic Data This Week (6/22--6/28)

United States (Core Themes: Inflation + Interest Rate Expectations)

Inflation Continues to Run at High Levels

PCE / Core inflation remains in the 3%--4% high range

The market's focus remains on core PCE stickiness (service + energy disruptions)

Inflation structure shows:

Energy temporarily receding

Service inflation remains strong

Core prices becoming "sticky"

Conclusion:

Inflation has not shown significant cooling, reinforcing the Fed's expectation of "higher rates for longer."

Consumption and Growth

Personal consumption and income continue to grow

The job market remains resilient

However, real purchasing power is suppressed by inflation

Conclusion:

The economy is "stable but not weak," in a typical soft-landing delay state.

Interest Rate Market Reaction

U.S. Treasury yields remain high and volatile

Market expectations for rate cuts continue to be pushed back

FedWatch pricing is leaning hawkish

2. Key Data Release Points for Next Week (6/29--7/5)

United States

1. Non-Farm Payroll Data (NFP)

Time: Thursday (moved up due to the holiday)

Focus:

Employment growth

Wage growth

Unemployment rate

Market Impact:

Strong → Reinforces rate hike expectations / Strengthens the dollar

Weak → Rate cut expectations return

2. JOLTS Job Openings

Measures the strength of labor demand

Determines whether the job market is cooling

3. ADP Small Non-Farm

Provides early guidance on NFP direction

Source of high-frequency volatility

4. ISM PMI (Manufacturing / Services)

Determines whether the economy continues to expand

Services = Key leading indicator for inflation

V. Regulatory Policies

United States

Legislation on stablecoins and market structure continues to advance: Congress continues to negotiate around the "CLARITY Act" and stablecoin framework, with regulatory focus on market structure delineation (SEC vs CFTC) and unification of stablecoin reserve rules, but the legislative process remains uncertain due to political agendas.

Institutionalization path strengthens: Large traditional financial institutions continue to promote the construction of tokenized assets and trading infrastructure, with the regulatory attitude overall maintaining an "open but strongly compliant" direction.

European Union

MiCA enters full implementation phase: Member states accelerate the integration of CASP licenses and unified law enforcement, shifting focus to compliance for stablecoin issuance, cross-border service restrictions, and reserve regulation enforcement, officially entering a "strong regulatory operation period."

Digital Euro infrastructure promotion: The ECB is advancing the selection of payment service providers and DLT pilots, paving the way for the digital euro to enter the testing phase (leaning towards CBDC infrastructure construction).

United Kingdom

- Stablecoin regulatory framework continues to adjust: The Bank of England and FCA continue to optimize stablecoin rules, rebalancing between financial stability and innovation space, focusing on reserve ratios, issuance restrictions, and banking participation rules.

Hong Kong

- Regulation of stablecoins and RWA continues to strengthen: Continuing the trend from early June, Hong Kong continues to promote the stablecoin licensing system and RWA tokenization regulatory framework, focusing on strengthening issuer access and reserve transparency requirements (overall moving towards an institutional market).

Singapore

- Regulation continues to maintain a "licensing + risk list mechanism": MAS continues to manage the warning list for unauthorized platforms while strengthening KYC and cross-border service restrictions, with an overall direction of high compliance thresholds and low tolerance regulatory framework.

Japan

- Crypto financialization reforms continue to advance: Continuing to promote supporting rules around crypto asset ETFs and institutional investor participation mechanisms, Japanese regulation remains focused on capital marketization and tax system optimization.

Risk warning

Risk warning

Popular articles